A Submission to Government by the Irish South & West Fish Producers’ Organisation

The Irish South & West Fish Producers Organisation and Octavian Consulting have compiled a submission to Government on a strategy for action and investment in Ireland’s Seafood Sector. In the submission they set out a 12-point recovery strategy from now until 2025, covering three phases: industry survival (2021-2022), industry recovery (2022-2024) and, finally, industry growth and internationalization (2024-2025)

Summary

Ireland’s seafood sector industry has huge potential for sustainable, community-based recovery in coastal areas most affected by Covid-19. Under the National Development Plan and the Recovery Plan, it should be a prime candidate for investment:

- Carbon emissions from the fishing industry are a small fraction of those from other animal-based food production industries. Seafood also has significant advantages in promoting physical and mental health.

- The Seafood industry’s economic hinterland contains over half a million people. Compared to other coastal economies of Europe it has fewer economic opportunities such as mass tourism, commercial port activity or oil and gas exploration and support services. Fishing is one of the natural industries it has left.

- Relative to other animal-based food industries, Seafood is both climate and health-friendly and community and family-oriented. It is therefore ideal for promoting recovery and employment growth in those coastal communities that were already marginalized before Covid-19 and most affected by it and by Brexit.

Unlike most other sectors, seafood failed to benefit from Ireland’s pre-Covid recovery. Investment, employment and activity declined at a time when these were booming in other sectors between 2015 and 2019. Loss of access to fishing waters will reduce the catch from €251.6 million per annum to €208.6 million per annum. So even before Covid, the industry was set to shrink by one fifth. New fishing opportunities – particularly in high-value species like bluefin tuna and swordfish – must now be obtained to compensate for this. Ireland’s global reputation for sustainable food excellence and growing world and EU demand creates huge opportunities. Major investment is needed to increase value-added, as recommended in the 2014 Focusing the Future Report. 1.5 per cent of GNI. The scars of Brexit will be more permanent and harder to heal for fishing than for other sectors due to a loss of fishing waters, quotas and entitlement to catch fundamental stocks.

As other fishing nations adjust to a loss of access to British waters, they will divert their superior fleets to fishing in Irish waters. Ireland’s fleet needs significant investment to compete with this. Despite greater need– the need for fishing crews to share confined spaces – Covid aid to the fishing sector has been lower than other food sectors and poorly designed, with low industry take up. Investment in a sustainable, pandemic-resilient fleet is an urgent necessity. Consistent with the Government’s aim for a spatially balanced “town/village centered” recovery across all of Ireland, our fishing industry must be far more regionally balanced than is now the case.

- Between the €10.1 billion allocated to capital spending in Budget 2021 and the €3.4 billion National Recovery Fund, there are ample resources to invest in a sector that has seen far too little investment during the good times, as consistent with 2014 Shelman report.

- This unique and significant opportunity to invest in creating a vibrant, sustainable industry that drives healthier eating habits must not be missed. The absence of a substantive commitment to developing Seafood in the Marine Planning and Development Management Bill must be corrected immediately.

- Ireland’s fishing industry should not be disadvantaged due to the fact that negotiations for a new Government were ongoing when the European Maritime Fisheries Fund (EMFF) was increased by over €500 million in June 2020 to assist the industry in responding to Covid-19.

As well as ensuring Ireland’s fair share of EMFF funding enhancements, outdated legacy quotas and Total Allowable Catch restrictions must be revisited and reset in a fair and proportionate manner.

Union Hall

Why We Must Act Now

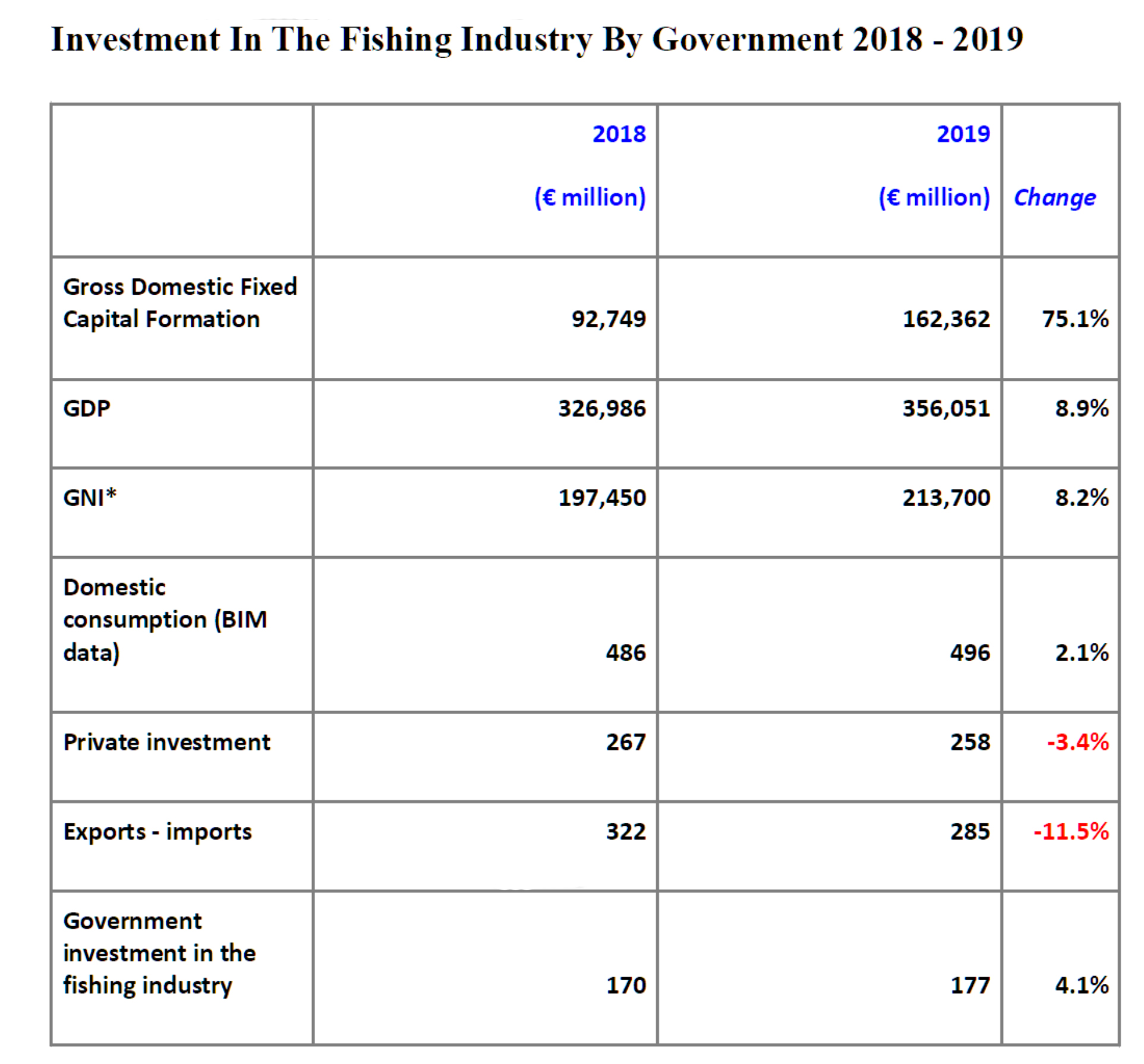

Rural and coastal Ireland is facing a crisis. A crisis of similar magnitude to the great depopulations of the past. Already denuded by the pull of urban Ireland, coastal communities have – despite a modest recovery pre-Covid – been further decimated by Brexit and the ravages of lockdown. Compared to other affected sectors, the Fishing industry has perhaps suffered the most because of its dependence on hotel and restaurant-led demand, the logistical difficulties of spatial distancing on fishing vessels, and decades of underinvestment and neglect. As the graph clearly shows, growth in investment in the fishing industry by Government in 2019 – despite strong growth in both GDP and GNI* measures of the economy – was half the rate of economic growth and very significantly short of overall investment in the economy. As a result, the industry has suffered in several ways:

Falling Trends

- In a year where GDP rose significantly, Ireland’s seafood GDP fell by 2 per cent year-on-year in 2019, from €1.25bn to €1.22 bn (Bord Iascaigh Mhara, 2020).

- From 2,127 vessels in 2018 the fishing fleet shrank to 2,022 in 2019, or by 4 per cent (Bord Iascaigh Mhara, 2020). The number of polyvalent boats over 18 meters in length had already fallen from 280 to 164 between 2006 and 2016 and is now set to fall even further as a result of reduced quotas and opportunities for Irish Fishers.

- Compared to a 3.5 per cent rise in overall employment, direct fishery employment fell from 3,231 to 3,033 in 2019, or by 6.1 per cent (Central Statistics Office, 2020).

- In contrast to a €69.6bn, or 75 per cent, rise in overall annual investment flows in the Irish economy during 2019, investment in seafood fell from €267m to €258m in 2019, a fall of 3.4 per cent (Central Statistics Office, 2020)(Bord Iascaigh Mhara, 2020). Net exports declined from €322m to €285m in 2019 in contrast with most other sectors.

These trends preceded the impacts of Brexit and Covid which have, since 2019, wreaked further devastation:

Brexit

- Whereas other sectors will suffer mostly transitional – although serious – impacts from Brexit, the seafood sector’s loss of access to UK waters is existential and permanent. As well as reduced capacity to generate raw material, this brings more EU vessels into Irish waters, displacing Irish vessels in our own waters and drastically cuts Fishing opportunities for Irish Fishing vessels in both UK and Irish waters.

- The agreement of December 24th 2020 with the UK poses significant uncertainty as it only lasts for five and a half years. Long-term investment requires a more permanent approach.

- The contrast with Brexit supports given to the beef industry is marked and – given the greater healthiness and climate friendliness of fish compared to meat – inconsistent with the PFG.

Covid-19 recovery

- Factors including confined spaces on fishing vessels and the fact restaurants and hotels are a major buyer of fresh fish (and therefore the closure or partial closure of these businesses has had a significant impact on demand), makes the impact of Covid on seafood more existential.

- The contrast with Covid supports to the beef industry is instructive as is the failure of the Temporary Tie Up scheme to attract any significant degree of industry buy-in.

- Involving industry representatives in designing measures to drive the recovery is imperative. A clear and spatially balanced industry stakeholder dialogue is needed to drive policy.

In 2014 the Shelman Report recommended investment in Ireland’s seafood industry to improve its scale, increase its quantity of value-added products, and expand its global reach. As the analysis above demonstrates, these recommendations were – despite robust recovery and tax resources between 2014 and 2019 – never realised. This must now be rectified as a matter of priority. The fundamental reason for this failure to drive investment in Ireland’s Seafood industry is grounded on the unmentionable – we are precluded from growing our own industry and availing of the wealth around our own coastline as a result of Common Fishery Policy of “Relative Stability” embedded since 1983. This protects coastal communities of the EU mainland that – unlike Ireland’s coastal economy – enjoy other sources of economic advantage. Instead of punishing Europe’s most peripheral coastal economies, policy should assist them.

It shouldn’t be happening

For several reasons, Ireland’s seafood industry is one of vast potential:

- Ireland’s geographical position means our waters stretch to the continental shelf. This means we have the most productive fishing waters in Europe, if not the entire northern hemisphere.

- Ireland’s global reputation for producing fresh, sustainable and safe food produce, and our significant coastline of clean, accessible seawater.

- EU per capita consumption of fish is, at 24.4 kg per person per annum, low by global standards (European Market Observatory for Fisheries and Aquaculture Products, 2020).

- EU consumption convergence with global norms will lead to growth in demand. With 20 per cent of EU waters, Ireland is well placed to serve this need if investment in upscaling and technology is made.

- Irish consumption (23.1 kg per person per annum) is lower still, and well below potential. Targeting increased fish consumption is environmentally sustainable. Fish consumption is also healthier and more consistent with Paris Climate targets (see chart).

With natural advantages other EU countries do not enjoy, and with the potential and need (for human health and climate action reasons) to increase European fish consumption, Ireland is ideally positioned to lead Europe in responsible, sustainable fishing.

The enhancement of the European Maritime Fisheries Fund (EMFF) in June 2020 occurred before Ireland had formed a Government. Government must now engage actively with the EU to ensure that Ireland retrospectively gets its fair share of the more than €500 million in additional funding that was allocated as a result of Covid-19. At the same time, the legacy of fixed Total Allowable Catch (TAC) and Quotas set in the 1980s must be addressed to put Ireland’s fishing industry on a level playing field compared to French, Dutch, Belgian and Spanish fleets.

Union Hall

Sustainable & Diverse Recovery

As a leading study (Parker, April 2018) shows, global fisheries account for just 4% of carbon emissions related to total food production and the carbon footprint of CO2 emitted per kilogram of protein is substantially lower for fishery products than for pork, lamb or beef. And yet, compared to investment in Ireland’s beef and dairy sector, far less environmentally sustainable sectors, fishery remains substantially under-invested in. Investing in Ireland’s fishery industry is therefore essential to securing the Programme for Government’s (PFG) commitments on achieving carbon neutrality by 2050 as targeted by the 2020 Climate Change Bill. The PFG commits to, among other areas, the following:

- Carbon emission reductions to achieve carbon neutrality by 2050.

- Developing a new integrated marine strategy

- Improving biodiversity

In several reports (Bord Iascaigh Mhara, 2018) Bord Iascaigh Mhara has stressed the importance of and potential for Ireland’s seafood industry to advance the agenda of environmental sustainability. Initiatives such as the promotion of Origin Green in the industry, organic certification, fishing for litter and co-ordinated aquaculture management systems demonstrate a growing commitment to preserving the environment that needs now to be matched by a commitment to preserving jobs. However in its recent report to government, the National Biodiversity Forum has highlighted the potential damage to biodiversity from our food industry. The Fishing industry will be a willing partner in this but success in this area requires investment and consultation as well as action by industry. Ireland’s strong commitment to environmental sustainability means it is imperative that we show an example to other EU member states by leading the responsible fishing of Irish waters. This requires investing in Ireland’s fishing fleet. The Programme for Government (PFG) has stressed the importance of focusing not only on economic goals as a metric of success, but on quality-of-life indicators, including public health.

Successive studies have shown that the benefits of eating fish include increased brain capacity, benefits to unborn children, and a possible reduction of risk for a range of disorders, including dyslexia, dyspraxia, Alzheimer’s, dementia and depression (Bord Bia, 2020). According to one study, over half a million people in the Republic of Ireland inhabit Ireland’s coastline economy (Curtin, 2018). This significant population is equivalent to the population of Dublin city. It is dispersed however and therefore benefits less from Ireland’s success in Foreign Direct Investment (FDI) and from other industries where population clustering is an advantage. Unlike the coastal economies of other countries – Portugal, Spain, Belgium, the Netherlands, and France – these coastal populations do not enjoy the advantages of climate, in terms of facilitating large tourist industries (as in Spain or Portugal) or geographical advantages that facilitate economic and commercial ports (as in Belgium and France). As well as being deprived of the advantages of their peers in other coastal parts of Europe, these communities are now witnessing the removal of oil and gas exploration and storage as an economic activity.

Seafood and tourism activities related to the natural and marine environment, such as Agri-tourism, together constitute the one single advantage and chance for economic survival that these communities have left. They must not have that taken away as well. As well as being environmentally sustainable and healthy, the seafood industry is also diverse in more than one respect: It is one of Ireland’s most diverse food sectors in terms of the destination of its exports. It is also an industry committed to gender diversification. Last but not least, it is part of a marine economy that has vast potential to diversify its product base into higher, value-added branded products, ranging from processed foods to cosmetics and health products. While dependent to a significant degree on UK waters for access to fishing waters, the fishing industry is far less dependent than other sectors on UK markets.

In contrast to meat products, which depend upon the UK for almost half of all exports (CSO), fishery exports to the UK constitute a significantly smaller proportion of total exports. Another encouraging factor for Ireland’s seafood sector is the recent growth in exports to Asia, where per capita consumption is significantly higher than in the rest of the world. Asia’s – and particularly China’s – growing economic importance, together with the post Covid-19 heightened consciousness of the importance of healthy and sustainable fish produce, presents Ireland with a significant opportunity to expand production and exporting. Through the “Women in Seafood” initiative of Bord Iascaigh Mhara, the seafood industry has consciously embraced and is pursuing the objective of gender diversity. By growing and investing in this sector, Government can provide more women with the opportunity to participate in a natural, sustainable, community and family-oriented industry.

If Government invests in upscaling, and research and innovation – to improve the industry’s value-added – then there is enormous potential for seafood to become part of an integrated maritime economy, encapsulating not just fresh fish, but, increasingly, high, value-added processed fish, cosmetics, and health products of strong appeal to high-income consumers. Species diversity must also be enhanced. As species like bluefin tuna, albacore tuna, swordfish, sardines and anchovies migrate northwards, Ireland must be given a fair chance to access them in a sustainable way. The Marine Institute should update government and industry on the potential for sustainable development of these species.

The IS&WFPO welcomes any comments or observations on our submission. Please email to info@irishsouthandwest.ie

Recent Comments